This article was recently published on Silly Investor's blog and is republished with permission.

BOTH Straco and UMS were on my radar screen when they were some 30% to 45% lower than their current prices.

That means I lost 50% to 90% of gains.

I was alerted to Straco when it was trading at 28 cents. I owned UMS at 37.5 cents but sold early at 44 cents.

It is perhaps important to review why I gave them a miss and learn some lessons.

Shanghai Ocean Aquarium is the key operating asset of Straco Corp. Shanghai Ocean Aquarium is the key operating asset of Straco Corp. Photo: www.shanghaifocus.com Straco Corporation: It is an S-chip, I had doubts about its numbers, especially when a blogger highlighted the low depreciation of its bio assets. |

UMS Holdings: Not an S-chip, it offered a dividend yield of more than 10% when I bought it.

I was aware of its FCF strength and the cyclical sector it is in. I was also aware of its heavy reliance on Applied Materials (AMAT) for profits.

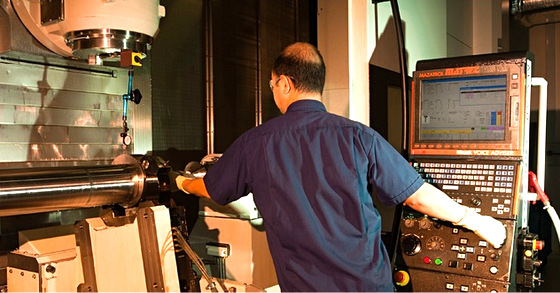

But I believed I got it with a good margin of safety.  UMS manufactures components and systems for semiconductor equipment. Photo: Company

UMS manufactures components and systems for semiconductor equipment. Photo: Company

Why did I sell? Because the owners, Andy and company, were selling a significant stake in the company, and it was the second time they did it in a year.

The first selling sparked the price fall which allowed me to collect on the cheap.

I was still hanging on to my shares when the news broke, and then shortly it was announced that Andy’s wife would cease to be a director and would be reassigned a consultant role instead.

This move did not make sense to me -- how effective can an insider be as a consultant or is already not a consultant?

I decided to bail out.

Well, on hindsight, it was a wrong call. I am fine with my decision as money not made is better than money lost.

But I think I will really should pay more attention to FCF growth, and if a stock sell-off is not too frequent or big such that the ownership of management comes into question, I should keep my steel.

FCF growth may or may not result in dividend growth, and it will take 1-2 years to find out how friendly management is to minority shareholders, but there is a good chance of higher dividends in both Straco and UMS as they are debt free.

Previous story: Investor: "Hard lessons learnt after my 2013 portfolio gained only 3.3%"

Chairman Mr Wu and wife are Singaporeans and the controlling shareholders. Mr Wu founded Straco. He was born & bred in SG, and graduated with a Bachelor of Commerce degree from the former Nanyang University (Singapore).

His wife, Madam Chua, was from the same university and same course.

http://www.stracocorp.com/directors.html