OSK-DMG maintains 'buy' call and 88-c target for Centurion

Analysts: Jarick Seet & Terence Wong, CFA

Centurion has established Oriental Amber Sdn Bhd. a new associated company in Malaysia with 49% interest and the remaining held by Mr Beh Pang Keat. On June 5th 2014, Oriental Amber has entered into a sale and purchase agreement to purchase a 7.6 acre freehold land in the Mukim of Jeram Batu, Johor Bahru, Malaysia for SGD4.55m.

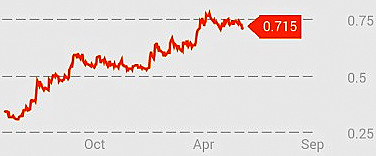

Centurion's shares have gained 114% in value in the past year.

Centurion's shares have gained 114% in value in the past year. Chart: BloombergThe acquisition is expected to complete within 3 months from the date of the SPA. The land is currently zoned for agricultural use, but can hold up to potentially 10,000 workers with 2 workers dormitory of about 5,000 workers each, subject to conversion to industrial use.

It is also located in Nusajaya district, one of the five flagship zones of Iskandar Malaysia and is in close proximity to several major industrial hubs such as Eco Setia Industrial Park, Southern Industrial and Logistics Clusters as well as Ascendes-UEM integrated Tech park.

This acquisition is in line with the group's strategy to expand its overseas dormitory business and would add an estimated SGD0.8m to the groups recurring profit when it is 100% occupied.

We maintain our BUY call with a SGD0.88 TP.

|

(YZJSGD SP/BUY/S$1.04/Target: S$1.39) FY14F PE (x): 6.4 FY15F PE (x): 6.2

target. As the capacity has been fully booked into 2016, YZJ has turned conservative and only targets orders with higher margins and more favourable payment terms. Maintain BUY with target price of S$1.39 unchanged, based on 1.3x 2014F P/B. YZJ has proven its leadership among non-SOE shipyards throughout the past years with its strong order winning/project execution capability and robust balance sheet. |