|

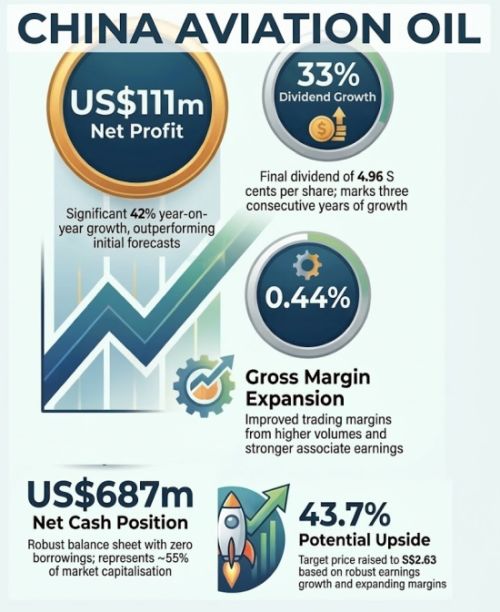

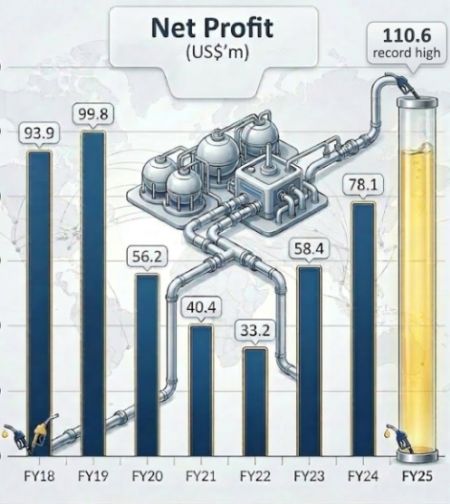

China Aviation Oil (CAO) surprised with a US$111 million net profit for FY2025, prompting a spate of analyst target price upgrades.

|

However, CAO is not gambling on these price swings.

CAO says explicitly it avoids short-term speculative trading and will instead adhere to its established, disciplined trading approach.

To navigate the turbulence safely, management has proactively conducted scenario analyses to evaluate the impact of the current geopolitical conflicts, allowing them to adjust trading strategies as needed to manage risk alongside the volatility.

CAO delivered a strong performance in 2025, reporting a record net profit of US$111 million, alongside expanding trading margins from higher volumes and future potential from the growing Sustainable Aviation Fuel (SAF) segment.

Other Merits Powering the Stock

UOB KH analysts highlighted several other merits that make CAO an attractive investment:

- Strong Associate Contributions: A significant chunk of CAO's earnings growth comes from its associates, particularly the Shanghai Pudong International Airport Aviation Fuel Supply Company (SPIA), in which CAO holds a 33% stake.

Associate profit contributions rose 31% year-over-year to US$60.2 million in 2025, providing reliable, recurring income that reinforces long-term cash flow stability. - Air Travel Recovery: The company is a direct beneficiary of the ongoing rebound in the aviation sector.

China's international outbound flights have recovered to over 90% of 2019 levels as of FY25, and the Civil Aviation Administration of China (CAAC) expects passenger volumes to climb 5.1% to 810 million in 2026, fueling consistent jet fuel demand.

CAO's profit in 2025 not only marks a third consecutive year of growth but also an all-time high for the company.

CAO's profit in 2025 not only marks a third consecutive year of growth but also an all-time high for the company.

|

OCBC Investment Research analyst Ada Lim raised her fair value estimate from SGD1.60 to SGD2.48.

This is pegged to a higher FY26 target price-to-earnings (P/E) ratio of 15.7x, which is roughly one standard deviation above CAO’s five-year historical average.

She considers a deployment of cash through accretive acquisitions or share buybacks to be one possible catalyst for the stock. → See also: Two China Stocks With Attractive Fundamentals Lead UOB KH's Alpha Picks Line-up

→ See also: Two China Stocks With Attractive Fundamentals Lead UOB KH's Alpha Picks Line-up