|

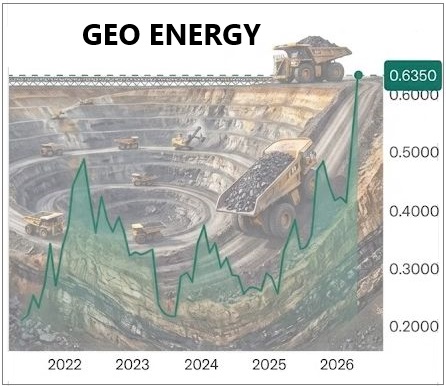

In the past week, Geo Energy Resources reached and sustained a market capitalization exceeding S$1 billion — driven by a convergence of rising cash flows from higher coal prices and structural milestones. |

How 2 brokers view Geo Energy:

|

Metric (FY26F) |

KGI |

Phillip |

Variance Notes |

|

Revenue (US$m) |

650.6 |

573.0 |

|

|

PATMI (US$m) |

71.5 |

56.8 |

Differing tax rate assumptions (25% vs 30%). |

|

DPS (SG Cents) |

1.9 |

1.3 |

KGI assumes higher payout on infrastructure scaling. |

|

Target price (SGD) |

$1.02 |

$0.75 |

| A Billion-Dollar Validation |

On April 15, 2026, Geo Energy closed at S$0.615, marking its position as a billion-dollar company.

This looks like a fundamental re-rating.

During the peak Covid years, ICI4 coal prices were even higher at ~US$100 and Geo Energy was hugely profitable.

The market is finally pricing in the MBJ Integrated Infrastructure project.

"With the Group recently achieving a market capitalisation of over S$1 billion, we are now ready to scale new heights with the upcoming completion of the MBJ Integrated Infrastructure and the ramping up of TRA coal production" "With the Group recently achieving a market capitalisation of over S$1 billion, we are now ready to scale new heights with the upcoming completion of the MBJ Integrated Infrastructure and the ramping up of TRA coal production"-- Charles Antonny Melati, Executive Chairman & CEO, Geo Energy |

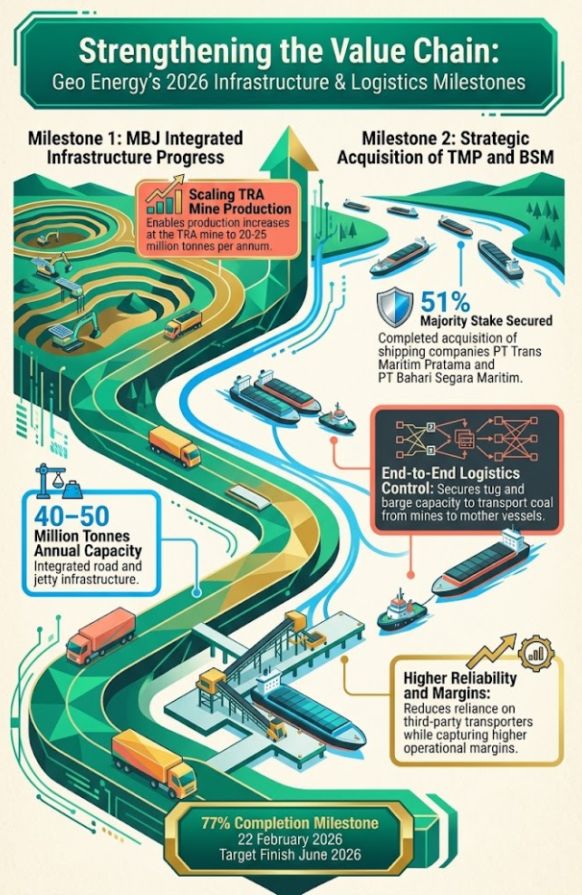

Currently at 90% completion, the 92km hauling road and jetty in South Sumatra is the ultimate "moat."

By owning the logistics chain, Geo Energy will slash its own operating costs by an estimated US$10 per tonne.

Importantly, it has secured binding agreements for 9 million tonnes of third-party haulage.

At full capacity of 50 million tonnes per annum, this infrastructure alone could generate up to US$300 million in EBITDA, transforming the company into a landlord with recurring, toll-based revenue.

| Strategic Diversification: The Coking Coal Play |

Adding fuel to the fire is Geo Energy’s recent foray into the high-value coking coal market.

The acquisition of a 50.6% stake in PT Mutiara Hitam Sukses marks a departure from thermal coal into the premium steel-making sector.

With coking coal fetching between US$220 and US$250 per tonne, the margins are night-and-day compared to thermal coal.

Geo Energy projects that this asset -- currently pre-production -- could contribute an additional US$220–$280 million in annual cash profits once production ramps up.

|

Metric |

Details |

|

Acquisition Stake |

50.61% of PT Mutiara Hitam Sukses |

|

Indicative 2P Reserves |

20 – 25 Million Tonnes of Hard Coking Coal |

|

Selling Price of Coal |

US$220 – US$250 per tonne |

|

Annual Production |

2 Million Tonnes |

|

Cash Cost |

~ US$110 per tonne |

|

Cash Profit Margin |

US$110 – US$140 per tonne |

|

Annual Cash Profits |

US$220 Million – US$280 Million attributable to Geo Energy |

This diversification significantly reduces the group’s risk profile and aligns it with the global demand for metallurgical coal required for green-energy infrastructure (like wind turbines).

|

→ See also: GEO ENERGY’s Transformation: Nothing like the past decade

→ See also: GEO ENERGY’s Transformation: Nothing like the past decade