|

The RHB "20 Jewels 2026 Edition" report has been released, spotlighting the top Singapore small-cap companies. The 2026 portfolio is anchored around three core pillars: international and regional growth, the technology value chain, and domestic structural trends. |

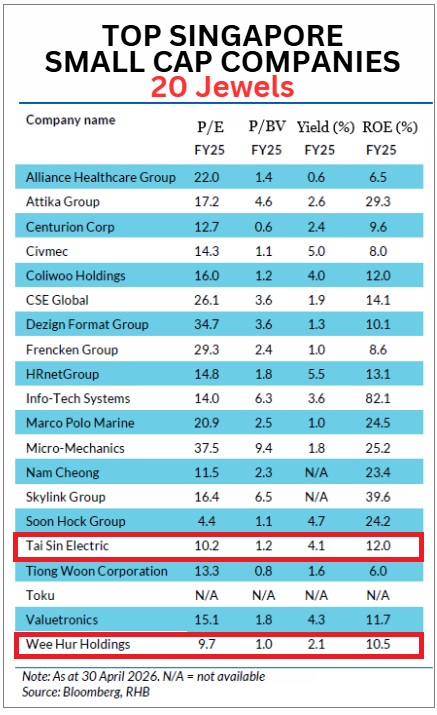

| Tai Sin Electric: Wired for Unprecedented Growth |

Tai Sin Electric stands out as a prime beneficiary of Singapore’s sustained construction boom and the rapid expansion of data centres (DCs).

RHB analyst Syahril Hanafiah notes: "The Building and Construction Authority projects Singapore's 2026 construction demand to remain strong." Tai Sin, a crucial player in digital infrastructure, has historically benefited from mega-projects and "remains well-positioned to capitalise on this ongoing construction boom".

Tai Sin, a crucial player in digital infrastructure, has historically benefited from mega-projects and "remains well-positioned to capitalise on this ongoing construction boom".

Hanafiah highlights that the company is "leveraging on regional presence amidst DC wave," adding that as a "dominant cable supplier having served 70% of DCs in the country, TSE is well-positioned to benefit from this expansion".

Hanafiah states: "Its strong domestic track record, dominant position in DC cable supply, and growing exposure to RE (renewable energy) and EV (electric vehicle) infrastructure provide diversified and multi-year growth drivers".

He emphasises the stock's compelling valuation, noting that it "only trades at 10x P/E, below the regional peer average of 25x".

| Wee Hur: Locked and Loaded for Re-Rating |

Wee Hur Holdings is riding also on Singapore's construction super-cycle and the need for foreign worker accommodation.

RHB analyst Shekhar Jaiswal describes the stock as being "locked and loaded for re-rating".

| Worker accommodation demand |

"The new regulations under the Dormitory Transition Scheme (by 2030) and New Dormitory Standards (by 2040) should structurally tighten supply. This regulatory tailwind, coupled with robust construction-driven demand for foreign workers, should position Wee Hur to sustain high occupancy and capture a low to mid-single-digit annual rental growth." "The new regulations under the Dormitory Transition Scheme (by 2030) and New Dormitory Standards (by 2040) should structurally tighten supply. This regulatory tailwind, coupled with robust construction-driven demand for foreign workers, should position Wee Hur to sustain high occupancy and capture a low to mid-single-digit annual rental growth."-- Shekhar Jaiswal, analyst |

He observes that the ramp-up of its new Pioneer Lodge dormitory "delivers a step change in recurring revenue".

On the construction front, Jaiswal notes that Wee Hur's record projected construction orderbook provides multi-year earnings visibility through FY31.

"We think Wee Hur is well positioned to be selective, prioritising margin-accretive contracts rather than chasing volume".

Furthermore, Jaiswal draws attention to "undisclosed value yet to be reflected in consensus estimates," citing assets like the Upper Thomson GLS project and Australian land subdivisions.

He views these impending disclosures as a "re-rating catalyst as the market gains visibility on these earnings streams".

Ultimately, Jaiswal concludes that Wee Hur "combines defensive dormitory income with a construction super cycle upside," while trading at an attractive 9.7x trailing P/E compared to its accommodation peers.

Both Tai Sin Electric and Wee Hur Holdings encapsulate the spirit of the RHB 20 Jewels report. |

→ See also:Why a Swiss Investor Just Valued One Piece of GEO ENERGY at US$1.5 Billion

→ See also:Why a Swiss Investor Just Valued One Piece of GEO ENERGY at US$1.5 Billion