|

Excerpts from UOB Kay Hian report

Analyst: Adrian Loh

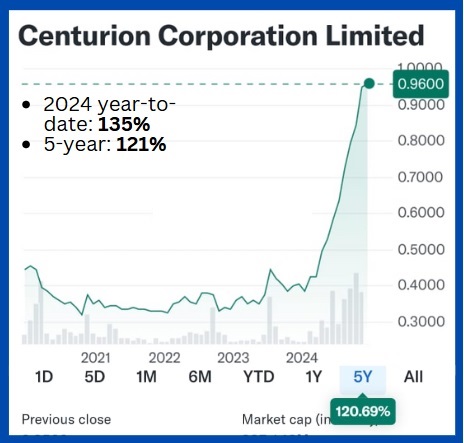

Centurion Corporation (CENT)

A Stock To Accommodate Growth-Minded Investors

CENT reported stronger-than-expected 9M24 revenue growth of 25% yoy to S$186.5m, driven by continued strong occupancies and positive rental revisions across both of its business segments.

We upgrade our 2024-26 EPS by 2-11%. Maintain BUY. Target price raised to S$1.11. |

||||

WHAT’S NEW

• Handily beating expectations again. Centurion Corp (CENT) reported strong 9M24 revenue of S$187m (+25% yoy) which formed over 82% of our full-year revenue estimate.

Like its 1H24 results, the company’s strong performance was attributed to strong occupancy rates and healthy rental revisions across its portfolio of Purpose-Built Workers Accommodation (PBWA) and Purpose-Built Student Accommodation (PBSA) assets with revenue growths of 27% and 20% yoy respectively. ASPRI-Westlite Papan: This Centurion worker accommodation is strategically located near Jurong Island, home to more than 100 global energy and chemical companies.

ASPRI-Westlite Papan: This Centurion worker accommodation is strategically located near Jurong Island, home to more than 100 global energy and chemical companies.

• Solid growth outlook from a healthy pipeline – guidance remains bullish. As seen in the chart overleaf, CENT should see around 16% volume growth in both its PBWA and PBSA segments during 2H24-2H26.

On our estimates, around 66% of the growth will come from PBWAs in Singapore.

In addition, the company commented that it is currently exploring opportunities for a potential development of around 7,000 beds in Iskandar, Johor, which we believe depends on the progress of the Special Economic Zone.

• Consistent insider buying this year. In a positive sign of the company’s near- to medium term outlook, we note that its CEO and its co-chairman have consistently bought the company’s shares this year.

Between them, they have purchased 2.39m shares at prices of S$0.40-0.74/share between Mar and Sep 24.

• Potential for higher dividend payout. Recall that during its 1H24 results, CENT declared a dividend of S$0.015, implying a 26% dividend payout based on EPS of S$0.0577 from its core business operations.

We have maintained our current forecast dividend of S$0.03 for the full year, but we believe that there is a high likelihood of an upside to S$0.035 given the better-than-expected earnings, implying a 2024 yield of 3.6% based on yesterday’s closing share price.

VALUATION/RECOMMENDATION

|

• Maintain BUY with a higher PE-based target price of S$1.11 (previously S$0.85) because of our earnings upgrades outlined above. |

Full report here.