|

Amid Singapore's ongoing construction boom, Tiong Woon Corporation (TWC) seems like an overlooked beneficiary, a kind of boring, unloved business. |

TWC offers another advantage -- instead of dealing with the hassle of hiring and coordinating several different contractors, customers hire just one company that has all the tools to handle the entire job from start to finish.

Even though the stock ($1.04) has risen 79% in the past year, it trades at undemanding valuations.

It is not lacking in analyst coverage, and its merits includes a strong balance sheet -- an uncommon trait among construction companies.

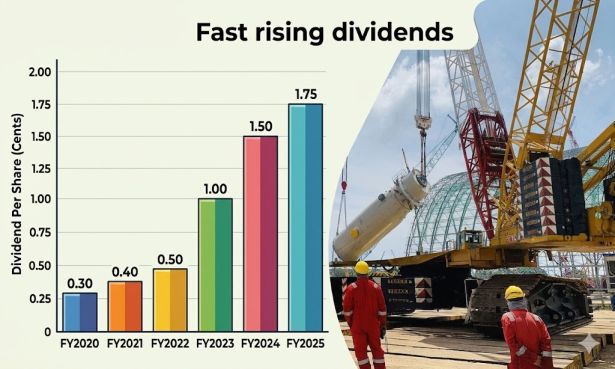

Heavy machinery is a capital-intensive business, and many companies drown themselves in debt. But not TWC.

"TWC is a cash-generative business with a low net debt balance sheet," as RHB analyst Alfie Yeo notes.

Aunique feature: TWC is the only heavy-lifting crane company in Southeast Asia that you can buy shares of on the public market. All of its competitors are privately owned businesses.

|

Analyst / Research Firm |

Date of Report |

Target Price (S$) |

|

Natalie Ong (CGSI) |

March 3, 2026 |

1.29 |

|

Lim & Tan Securities |

Jan 30, 2026 |

1.30 |

|

Alfie Yeo (RHB) |

May 2026 |

Not rated |

Let's see what analysts say:

Natalie Ong from CGS International points to TWC’s shift toward higher-value, integrated heavy-lift projects.

In her March 3, 2026 report, she notes that TWC's involvement in complex petrochemical, oil and gas (O&G), and data center installations helped push gross profit margins from 38.5% in 1HFY25 to an impressive 42.9% in 1HFY26.

She highlights Singapore's domestic project pipeline, including the Micron Technology wafer facility and Tuas pharmaceutical projects, as key drivers for near-term fleet utilization.

Lim & Tan Securities, in its Jan 30, 2026 Daily Review, emphasizes TWC's international growth as the real source of "earnings alpha".

The broker highlights that TWC is deploying high-tonnage cranes to overseas projects—such as the NEOM mega-project in Saudi Arabia and petrochemical facilities in India—which carry higher margins.

| Fair value $1.30 |

| "If we ascribe an undemanding 12x PE (which we think is fair given construction majors BRC Asia/Centurion also trades at around 12x forward PE and Pan United/Hong Leong Asia trades at around 18x PE), TWC should trade at S$1.30 given its status as a crane major." -- Lim & Tan Securities |

Lim & Tan also views TWC’s recent acquisition of Mammoet’s assets in Thailand as a testament to its competitive edge, noting that even global giants are choosing to divest regional assets to TWC.

Alfie Yeo from RHB, who included TWC in the broker's "Top 20 Singapore Small Cap Jewels 2026," approaches the thesis from a macro-demand angle.

He notes that TWC is a direct beneficiary of high global oil prices, which are incentivizing producers to increase supply and ramp up O&G extraction activities.

Notably, "as a crane rental company, it is not exposed to tender price and labour cost pressures unlike the main contractors. Its operating model is largely based on a return on its assets leased, which is more stable than pure-play construction companies."

The investment thesis for Tiong Woon is multifaceted. |

→ See also:NORDIC: Cash-Positive Again and Piling Up $: What Are Growth Areas for This Company?

→ See also:NORDIC: Cash-Positive Again and Piling Up $: What Are Growth Areas for This Company?