|

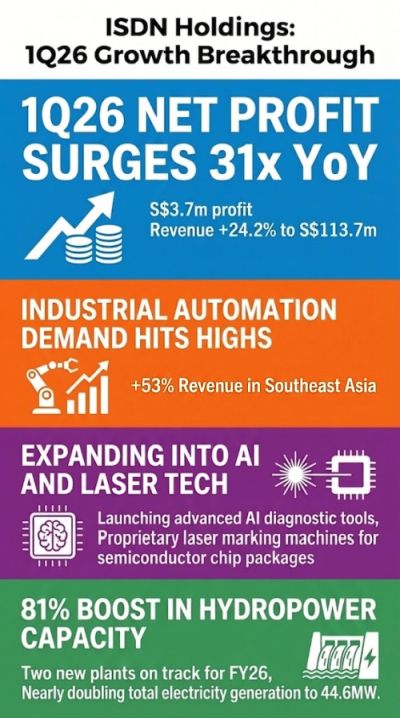

ISDN Holdings has delivered a strong set of results for 1Q 2026 riding the wave of a recovering semiconductor industry and capitalizing on strategic shifts in global supply chains. It reported a 24.2% year-on-year surge in revenue to S$113.7 million, which drove a turnaround in profitability, with net profit rising to S$3.7 million from S$120k.

|

| Growth Drivers: Semiconductors and Strategic Investments |

1Q was largely powered by ISDN's industrial automation segment, which saw revenue growth of 23% year-on-year, including a 53% leap in Southeast Asia. This surge is heavily tied to the upturn in the semiconductor equipment manufacturing sector across the region.

During the 2021-2023 industry downturn, ISDN proactively expanded its capabilities. As Managing Director CK Teo explained at an earnings call, "we beefed up our capability. We invested in a better injection molding factory... and we expanded our business in Malaysia, ready for the upturn of the semiconductor industry".

ISDN is also capturing market share with innovative solutions like its new IDI laser marking machine, which resolves critical space and speed constraints for outsourced semiconductor assembly and test (OSAT) companies.

According to Mr. Teo, this proprietary machine is "2.5 times faster than the peers' and it saves a lot of space in the clean room".

Analyst Perspectives & Geopolitical Tailwinds

|

ISDN |

|

|

Share price: |

Target: |

Analyst William Tng highlighted in his post-1Q report: "ISDN is benefitting indirectly from the global growth in AI, data centres, semiconductors and energy storage, as it supplies a broad range of components and solutions to these sectors."

He reiterated an "Add" rating on the stock with an unchanged S$0.96 target price, stating, "we expect earnings growth to resume over FY26-28F" with a projected EPS compound annual growth rate of 45.6%.

He also pointed to potential re-rating catalysts, such as "a stronger global semiconductor recovery" and higher profit contributions from the hydropower segment.

| Year of harvest |

"I'm very excited, I'm happy with the results so far and with what I've seen, with what I hear from the ground. And I think this year we can really harvest. So I hope to bring more good news to the market, to the shareholders ..." "I'm very excited, I'm happy with the results so far and with what I've seen, with what I hear from the ground. And I think this year we can really harvest. So I hope to bring more good news to the market, to the shareholders ..."-- CK Teo, MD of ISDN Holdings |

This technological momentum is amplified by the "China Plus One" strategy, which is pushing massive foreign direct investment into Southeast Asia.

Mr. Teo pointed out that "ASEAN now emerged to be the largest trading partner of China", positioning ISDN to capture the resulting automation demands in these expanding regional manufacturing hubs.

Renewable Energy & A Record-Breaking Outlook

Beyond automation, ISDN's renewable energy pillar provides steady, diversified growth.

Revenue in this segment grew 39.3% year-on-year to S$6.7 million in 1Q2026, bolstered by construction income from two new mini-hydropower plants in Indonesia.

Once hydropower plants Lau Biang 2 and 3 are completed by the end of 2026, these facilities will expand ISDN’s total electricity generation capacity by 81% to 44.6 megawatts.

Looking ahead, ISDN’s management remains highly optimistic. The current momentum is very strong, with Mr. Teo referencing the company's order book being sharply higher than last year. CGS, the only covering broker, has forecasted strong EPS growth, as shown in the table:

Reflecting on the company's booming end-markets and 39-year streak of profitability, Mr. Teo closed the earnings call with confidence: "I think this year we can really harvest". The seeds the company planted during the downturn are going to bear lots of fruit? |

|||||||||||||||||||||||||||||||||||||||||||

→ See also:ISDN: This Stock Rockets 24% After Analyst Raises Target Price 2X

→ See also:ISDN: This Stock Rockets 24% After Analyst Raises Target Price 2X